Are we building data centers for AI—or something else? Data from the industry suggests a more insidious motive.

Data center developers pitch a future in which AI supercharges the economy and jurisdictions that fail to build capacity are left behind. Venture capitalists are tripping over themselves to back the premise that future demand will come primarily from generative AI research and applications.

Given the hype, you’d be forgiven for assuming that AI accounts for the overwhelming majority of data center usage. It doesn’t. Industry reports show AI representing only 20% of data center use (EPRI 2026). Of course that number is supposed to increase, but we’ve been hearing that for years now. What’s guzzling most of the electricity and water?

Many non-AI workloads are mundane, such as cloud storage and streaming video. But the most energy-intensive uses include crypto and ad targeting—tasks with little appeal for the average consumer.

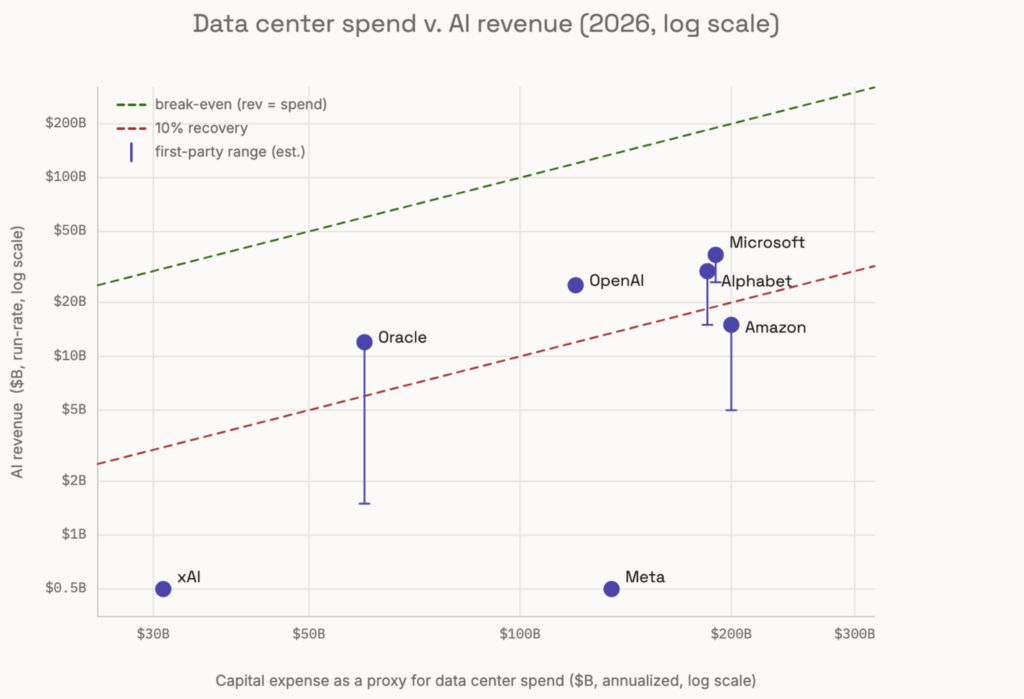

What if, as Joline Blais suggests with the phrase “AI Trojan Horse,” AI is helping justify infrastructure built not to serve humanity but to serve Ozempic ads? I decided to investigate this hypothesis by graphing how much companies are spending to build data centers compared to how much they make from their AI businesses. Plotted on logarithmic axis, the disparity is stark: most companies are recouping only around 10% of their data infrastructure expenses with AI revenue. This is true whether the company is AI-first (OpenAI) or conglomerate (Alphabet/Google) and whether it’s spending $30B or $200B.

Even more telling are graph outliers xAI and Meta, which are spending truckloads of cash on data centers despite their generative AI businesses being economic failures.

xAI bought a lot of GPUs in anticipation of renting them to other companies if their own AI ambitions didn’t pan out, making it the proverbial purveyor of shovels during a gold rush. For its part, Meta seems to be taking a different tack befitting its core business model of targeted advertising. When you’re literally tracking every time Jane in Poughkeepsie moves her mouse, that produces petabytes of data per hour that have to be processed somewhere. It’s easier to justify Meta’s awkward position in this space if you see it riding the AI hype to fund infrastructure that will also surveil users on Facebook and Instagram.

Some will argue that the companies with more skin in the AI game, like Alphabet and Microsoft, are positioning themselves to take advantage of generative AI in case it really does prove as transformative as boosters predict. Even for such deep pockets, though, that’s a lot of outlay for an uncertain payoff.

A more plausible hypothesis, I think, is that these companies are hedging: if the AI bubble bursts they will have still convinced venture capitalists and willing governments to fund their core business model of cloud computing and surveillance advertising. The AI label unlocks subsidies, fast-tracked permits, and “AI race” political goodwill. It’s a lot easier to justify flickering light bulbs and dripping faucets when the goal is powering AI breakthroughs rather than queuing up eating disorder reels on Instagram.

So the next time someone argues for building a new data center to usher in the AI Revolution, ask them what the other 80% is going to be used for.

Method

I am deliberately looking at a snapshot of today’s economy rather than speculating about future growth, eg by using current run-rates of AI companies and annualizing OpenAI’s multi-year “commitment.”

I used a logarithmic scale to show small AI labs and tech giants following the same trajectory of ~10% return from AI on data infrastructure.

I used capital expenditures as a proxy for data center spending for all the major players, typically based on trailing twelve months revenue from the most recent reported quarter. This assumption seems reasonable except for Amazon, whose value is probably inflated due to significant capex spent on physical storage and transportation.

The bottom of each vertical error bar strips out compute rented to other companies. In descending order of significance: Oracle rents to OpenAI/Stargate; Amazon rents to OpenAI; Alphabet sells chips to Anthropic; Microsoft mostly uses its own Azure cloud. OpenAI and xAI are exclusive users of their data infrastructure. Meta sells no direct AI product.

Claude Opus 4.8 helped with research and graphing.

Sources (verified by author)

- AI workloads account for 15–25% of 2026 data center electricity EPRI

- Microsoft FY2026 Q3 earnings; $37B AI run-rate, ~$190B 2026 capex, $82.9B quarter Microsoft Investor Relations

- Alphabet FY2025 annual report ($402.8B revenue) SEC / Alphabet ARS

- Alphabet Q1 2026 results (Cloud +63%) SEC / Alphabet 8-K

- Meta Q4/FY2025 ($200.97B) and Q1 2026 ($56.31B; 2026 capex $125–145B) Meta Investor Relations

- Amazon FY2025 net sales $716.9B / TTM $742.8B Stock Analysis

- AWS AI >$15B run-rate BNN Bloomberg

- Oracle Q2 FY2026 (OCI +68%, FY2026 ~$67B guide, capex raised) Futurum Group

- OpenAI CFO: $20B annualized revenue (2025) Yahoo Finance / Reuters

- OpenAI ~$25B revenue run-rate (Feb 2026) Sacra

- OpenAI $600B compute commitment through 2030 CNBC

- OpenAI Stargate walk-back from $1.4T to $600B; shift to leasing TechTimes

- xAI financials (SpaceX S-1): $3.2B 2025 revenue, $12.7B 2025 capex, $30.8B annualized; Colossus rentals to Anthropic ($1.25B/mo) and Google ($920M/mo) TechCrunch

- xAI standalone revenue run-rate ~$500M Sacra

- Big Tech 2026 data-center spending plans reach $725B Tom’s Hardware; Visual Capitalist